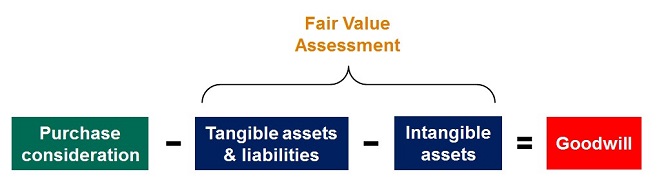

All Tangible and Intangible Assets,Liabilities and Goodwill in Merger and Acquisition Transaction

According to IFRS Standard 3, the acquirer, in a Business Combinations, shall recognise, separately from goodwill, the identifiable assets acquired, the liabilities assumed and any non-controlling interest in the acquire as of the acquisition date.

The acquirer shall identify the acquisition date, the date on which it obtains control of the acquire, which is generally the date on which the acquirer legally transfers the consideration, acquires the assets and assumes the liabilities of the acquiree—the closing date. However, the acquirer might obtain control on a date that is either earlier or later than the closing date. For example, the acquisition date precedes the closing date if a written agreement provides that the acquirer obtains control of the acquiree on a date before the closing date.

A transaction or other event in which an acquirer obtains control of one or more businesses. Transactions sometimes referred to as ‘true mergers’ or ‘mergers of equals’ are also business combinations as that term is used in this IFRS.

Copyright © 2024 AP Appraisal Limited. All Rights Reserved. Privacy Statement | Terms of Use